Best AI Personal Finance Apps 2026: Budget and Track

The best AI personal finance apps in 2026 reviewed: Cleo, Monarch Money, Copilot, Origin, YNAB, Rocket Money, and the new ChatGPT Plaid integration.

Bytewaves Score Card

Mint is gone, and its 22 million users are now split across a dozen apps that range from genuinely useful to marketing dressed up as AI. The question is not whether AI budgeting tools have improved since Mint's March 2024 shutdown. They have. The question is which one is worth your bank credentials, your monthly fee, and the behavioral follow-through required to make any budgeting app actually work.

I tested eight apps across a two-income household with a mix of fixed and variable expenses, two investment accounts, and the specific annoyance of forgotten subscriptions that compound quietly. Here is what the data shows, what actually matters, and which app fits which situation.

Quick pick: Monarch Money for most households. Copilot for Apple-only users who want the best categorization. Rocket Money if forgotten subscriptions are your main problem. Cleo if you are new to budgeting and want something that does not feel like a tax audit.

Why the AI personal finance app category finally matters in 2026

The Mint shutdown was not just a product death. It was an exposure of what the category had been. Mint used rigid rule-based categorization that mislabeled "WHOLEFDS #432" as "ATM/Cash" for seventeen years. It monetized user data through credit card and loan offers.

Its "AI" was a marketing label on a rules engine. That distinction matters when evaluating what is on offer now.

What replaced it is genuinely different. The best apps in 2026 use machine learning models that learn from your specific transaction patterns, not shared generic rules. Copilot achieves approximately 93% first-pass categorization accuracy using a per-user model that gets more accurate the longer you use it. Monarch's AI assistant produces weekly cash flow summaries grounded in your actual accounts.

Origin's AI Advisor can answer "is my spending affecting my retirement timeline?" using your real investment and savings data. That is a different category of tool than Mint ever was.

The 2025-2026 apps also tackle a broader problem. A Vanguard survey found 74% of Americans missed their saving and spending goals in 2025. Nearly 89% of consumers underestimate their subscription spending by 2.5x. Over 43% of Americans now use AI for some aspect of their financial planning (NerdWallet, 2026).

The tools exist. The gap is helping people choose the right one.

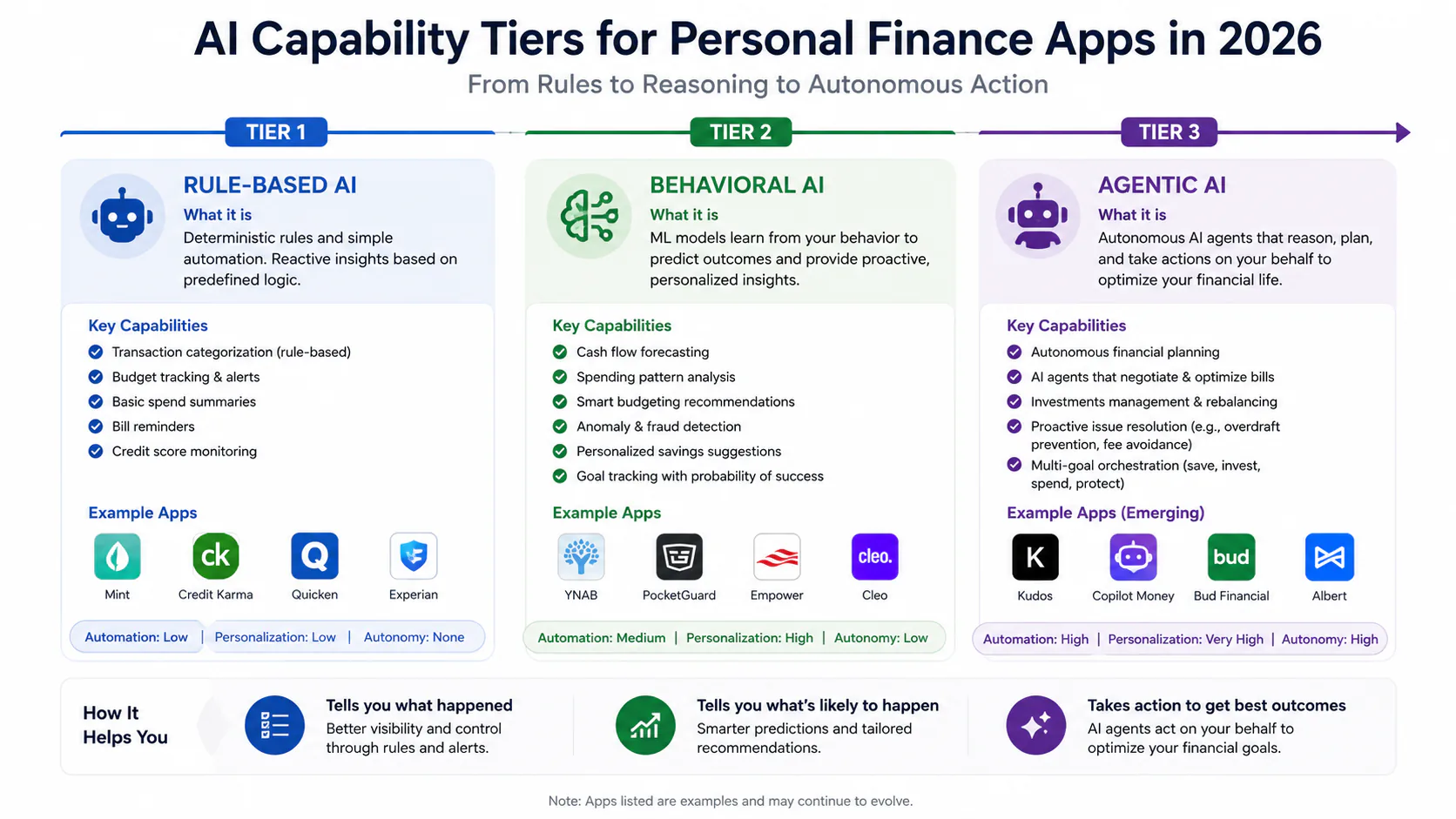

The three AI tiers you need to understand before choosing

Not all "AI" in finance apps works the same way. Three distinct capability levels determine what you are actually buying:

Tier 1, rule-based automation: Fixed categorization rules and scheduled alerts. The AI badge here is marketing. The tool does not learn from your behavior. Most legacy apps and some current free tiers operate here.

Tier 2, behavioral AI: Machine learning that trains on your transaction history over weeks and months. Improves recommendations based on your actual patterns. Copilot and Monarch Money operate at this tier. The key tell: if correcting a miscategorized transaction actually makes the same transaction categorize correctly next time, you are using real behavioral AI.

Tier 3, agentic AI: Pursues goals across multiple steps without human input for each one. An agentic money app can inspect your income variability, identify unused subscriptions, propose a savings plan, and automatically move money when a paycheck clears. Rocket Money's bill negotiation service and Cleo's Autopilot are early examples. Full agentic financial management is the direction the category is moving.

Understanding which tier each app operates at tells you what to expect from the "AI" in the feature list.

The eight best AI personal finance apps in 2026

Monarch Money: Best overall for most households

Monarch was built by the original Mint product team after Intuit's shutdown, and it shows. The interface is what Mint should have become: full-household financial visibility with AI that actually adds something.

The AI assistant sends weekly spending recaps and flags anomalies before they become problems. The net worth dashboard aggregates bank accounts, investment accounts, and liabilities in one view. Couples support is a genuine differentiator: Monarch handles "yours, mine, and ours" budgeting with shared goals and individual spending visibility on the same dashboard.

The limitation worth knowing: Monarch uses a mix of in-house and third-party large language models for its AI features. Their own documentation confirms this. Transaction text may be processed by LLM providers outside the app. For most users this is acceptable. For users with sensitive financial situations (pending litigation, professional licensing concerns), it warrants consideration.

Pricing: $14.99/month or $99.99/year (Core); $199/year (Plus). No free tier.

Copilot Money: Best AI categorization if you use Apple

Apple Editor's Choice. The most polished personal finance experience on the market, with one constraint that eliminates it from consideration for roughly half the audience: iOS and Mac only.

Copilot's per-user AI model achieves approximately 93% first-pass categorization accuracy. Each user has their own model trained on their specific transactions. When you correct a miscategorization, your model learns. After a few weeks, you will rarely see the same mistake twice.

This is the single most practical improvement over Mint's endless manual cleanup cycle.

The app does not use a chatbot interface. The AI works behind the scenes: categorizing, tracking subscriptions, and surfacing spending trends in a clean dashboard without requiring you to prompt it.

The hard limitation: No Android. No Windows. No meaningful web version. Single-user only, no couples sharing. If your household has mixed devices, or your partner is on Android, Copilot is not an option regardless of quality.

Pricing: $13/month or $95/year. No free tier.

Rocket Money: Best for subscription management

The highest-ROI first action for most households is a subscription audit. Most people believe they have eight active subscriptions. The NerdWallet 2026 survey puts the actual average at 12. The gap is $40-$80/month of charges that accumulated while you were not looking.

Rocket Money does one thing better than any other app: it finds those subscriptions, presents them clearly, and offers to cancel the ones you no longer want. The premium tier adds a bill negotiation service where Rocket Money contacts providers on your behalf and negotiates lower rates, keeping a percentage of the savings.

The comprehensive financial features (budgeting, credit monitoring, net worth tracking) are functional but not the reason to use it. Use it for subscriptions first.

The limitation: The flexible pricing model ($7-$14/month where you choose what you pay) sounds user-friendly but can make it feel ambiguous what you are getting at each tier. The core subscription detection feature is worth the lower end of that range.

Pricing: Limited free tier; $7-$14/month premium (you choose); $84-$168/year.

Cleo: Best for beginners and cash-flow-tight households

Cleo is the only app in this comparison that was deliberately designed for people who find traditional budgeting apps feel like a punishment exercise. The conversational interface is intentionally casual. The "Savage Mode" roast-style spending feedback is optional. The underlying financial capability is real.

Cleo's Autopilot saves money automatically by analyzing your income and cash flow patterns. When a paycheck clears, Autopilot moves a conservative amount to a savings buffer before you can spend it. This is the most powerful behavioral finance intervention available in any app: it removes the deliberate savings decision, which is where most people fail.

The cash advance feature (up to $500, no credit check, on paid tiers) is a practical safety net for households with variable income or occasional shortfalls.

The key limitation: Cleo's premium tier ($14.99/month, or $19.99/month for Cleo membership) costs more annually than YNAB but lacks investment portfolio management, retirement projection, or comprehensive financial planning. It is a coaching and cash-flow tool, not a full wealth platform.

Pricing: Functional free tier; $5.99-$14.99/month for paid features; cash advances on paid plans.

Origin: Best for wealth planning with AI reasoning

Origin occupies a different position than the other apps in this comparison. It is not primarily a budgeting tool. It is a wealth platform with budgeting built in.

The AI Advisor answers questions like "Is my spending affecting my retirement timeline?" and "Should I adjust my savings rate based on this month's cash flow?" It grounds those answers in your actual account data across investments, retirement accounts, liabilities, and cash flow.

For users in their mid-30s or older with real financial complexity (equity compensation, multiple retirement accounts, mortgage, variable income), this is a different category of insight. No standalone budgeting app provides retirement projection grounded in your actual accounts.

Couples access is included at no extra cost (unlike Monarch's separate pricing). The platform is built with integrated compliance checks and audit logging designed for financial guidance.

Pricing: Approximately $12-$15/month. Contact Origin directly for enterprise or family pricing.

YNAB: Best for behavioral change through discipline

YNAB is the oldest platform in this comparison and the only one where the core value proposition has nothing to do with AI. Zero-based budgeting is a methodology, not a data problem. Every dollar is assigned a job before it is spent. If you run out of dining budget, you have to consciously move money from another category to spend more.

YNAB added an AI layer in late 2025 for spending analysis and goal recommendations. The AI supplements the methodology rather than replacing it. The real product is the four-rule system and the engaged community that has built up around it.

YNAB reports users save an average of $600 in their first two months. That figure is corroborated by independent user communities and is the strongest empirical outcome evidence in the category.

The honest drawback: Abandonment rate is high. The methodology requires ongoing engagement. If you use YNAB the way most people use budgeting apps (check it once, ignore it for three weeks), you will get nothing from it. The commitment required is real.

Pricing: 34-day free trial; $14.99/month or $109/year.

Empower: Best free option for investment tracking

Empower is the only app in this comparison with a genuinely comprehensive free tier. The investment fee analyzer scans all linked accounts, identifies expense ratios, and calculates their 10, 20, and 30-year compound cost. A 0.5% expense ratio difference on $100,000 costs more than $7,000 over 20 years. Empower shows you that number.

The net worth dashboard aggregates bank accounts, investment accounts, and retirement funds in a single view. AI-powered spending trend analysis is included. No premium required for core features.

The tradeoff is the revenue model. Empower makes money by converting users with $100,000 or more in investable assets to its wealth management advisory service. Expect in-app messaging about financial advisors once your tracked net worth crosses that threshold.

Pricing: Free. Wealth management advisory available as a paid service for users who want it.

ChatGPT with Plaid: Best for open-ended financial reasoning

The most significant new entrant in the category launched in May 2026. OpenAI connected ChatGPT to Plaid, giving Pro subscribers the ability to have real conversations about their actual financial data.

The core differentiation is reasoning capability. Every app in this comparison answers fixed questions. ChatGPT with Plaid answers novel ones: open-ended scenarios that require reasoning across account balances, interest rates, upcoming bills, and your stated priorities simultaneously. No dedicated budgeting app handles that class of question.

The hard constraint: ChatGPT Pro is $200/month. That is $2,400/year for a budgeting feature. OpenAI has stated that financial data is not used for model training and that users can disconnect accounts and delete stored data. But at $200/month, this is not a mass-market product.

A ChatGPT Plus tier with Plaid integration is likely coming. Until it does, this is relevant for users who are already Pro subscribers for other reasons.

Pricing: $200/month (ChatGPT Pro only, as of June 2026); US only.

Full comparison table

| App | Best for | AI tier | Couples | Free tier | Annual cost |

|---|---|---|---|---|---|

| Monarch Money | Most households | Behavioral | Yes | No | $100-$199/yr |

| Copilot Money | Apple users | Behavioral (strong) | No | No | $95/yr |

| Rocket Money | Subscription audits | Rule-based+ | Limited | Limited | $84-$168/yr |

| Cleo | Beginners, variable income | Behavioral | No | Functional | $72-$180/yr |

| Origin | Wealth planning + AI | Behavioral+ | Yes (free) | No | ~$144-$180/yr |

| YNAB | Behavioral change | Rule-based + AI | Yes | 34-day trial | $109/yr |

| Empower | Investment tracking | Behavioral | No | Full free | Free |

| ChatGPT + Plaid | Complex financial Q&A | Full LLM | N/A | No | $2,400/yr |

Privacy: what connecting your bank account actually means

Every cloud-based app in this comparison connects your bank through Plaid, a financial data aggregator used by Venmo, Robinhood, and thousands of fintech apps. Plaid covers over 12,000 financial institutions. The connection is read-only for tracking apps. The exception is apps with auto-save features (Cleo Autopilot, Rocket Money auto-save) that require write permissions scoped to savings sweeps.

Plaid stores tokenized access rather than your raw credentials and uses AES-256 encryption. What it also does is retain your transaction data on its own servers. A 2022 class action alleged Plaid collected more data than users authorized. The company settled and updated its policies.

Three privacy tiers exist in the current market:

Cloud with third-party LLM processing (highest exposure): Monarch Money's documentation confirms it uses third-party LLMs for AI features, meaning transaction text may be processed by external providers. This is the privacy tradeoff for the best AI analysis.

Cloud with first-party processing only: Copilot's per-user model is more private by architecture: your data trains your model, not a shared model. Origin's compliance-first architecture includes audit logging and regulatory safeguards.

Local-first alternatives: Finny ($1.99/month) and SenticMoney ($39/year) store financial data on-device only. No Plaid, no cloud sync, no bank credential sharing. The tradeoff is manual data entry and no automated transaction import.

For most users, the Plaid tradeoff is acceptable. For users with sensitive financial situations, local-first tools are worth knowing about.

Pros and cons of AI personal finance apps (2026)

Pros

- AI categorization that learns from corrections reduces the endless manual cleanup that caused most Mint users to abandon the category entirely.

- Forward-looking alerts notify you before you exceed a budget category, while there is still time to adjust, instead of reporting it afterward.

- Subscription detection surfaces $40-$80/month in forgotten charges for most households on the first audit.

- Agentic auto-save features (Cleo Autopilot, Rocket Money) remove the friction of the deliberate savings decision, which is where most people fail.

- Wealth planning tools like Origin provide retirement projection and investment fee analysis that previously required a fee-only advisor at $200-$400/hour.

Cons

- Bank connection fragility is a chronic, unsolved problem. Plaid connections break after bank security updates. Expect occasional reconnection prompts and do not rely on automated syncing exclusively.

- Most apps have raised prices significantly since 2024. YNAB is now $109/year. Monarch is $99.99-$199/year. Apps that were free in 2022 now cost $12-$15/month. The cost of using a budgeting app adds up.

- AI cannot solve an income problem. The most common failure mode is not the app. It is downloading a budgeting app when you are financially stressed, then abandoning it when the data makes the stress worse. No app fixes that.

- "AI" labeling is inconsistent across the category. Rule-based alert systems and behavioral machine learning models are both described as "AI" in app store listings. The difference matters for whether the tool improves over time.

- No app provides regulated financial advice. Cleo, Monarch, Origin, and ChatGPT all explicitly state their AI responses are not personalized investment advice from registered advisors. Tax decisions, estate planning, and complex debt situations still require human advisors.

Who should use AI personal finance apps in 2026

Use one if:

- You have more than three bank or credit card accounts and no consolidated view of your spending.

- You have not done a subscription audit in more than six months.

- You are in a two-income household without a shared system for tracking shared expenses.

- You want forward-looking cash flow alerts rather than monthly reports of what already happened.

- You are post-Mint and have not found a replacement that actually stuck.

Skip the paid tiers and use Empower's free tier if:

- Your primary need is investment and net worth tracking, not budgeting.

- You want to see what your expense ratios are actually costing you over time.

- You are not ready to pay $100-$200/year for a budgeting tool before knowing whether you will use it.

Do not use any of these tools if:

- You need actual regulated financial advice. These are data tools, not licensed advisors.

- You are on Android and want Copilot's categorization quality. It does not exist on Android yet.

- Your primary goal is active investing decisions. These apps track spending and net worth; they do not replace brokerage platforms or investment research tools.

If you want a broader survey of where AI tools are useful across categories beyond finance, the free AI tools review for 2026 covers the landscape. For AI tools that go deeper on research and analysis, the NotebookLM 2026 review is a useful counterpoint on where AI reasoning actually delivers value.

Is it worth it?

For most households: yes, but pick by use case rather than by feature lists.

Monarch Money is the closest to a universal pick. It handles couples, investments, and budgeting in a single platform with real behavioral AI and a polished interface. At $99.99/year, it costs less per month than a single restaurant meal. The third-party LLM data processing is a known tradeoff.

Copilot is the best categorization experience available if you are in the Apple ecosystem and live alone or have a partner who also uses Apple. Its per-user model is the most privacy-preserving cloud option in the category.

Rocket Money earns its fee in the first subscription audit for most households. Use it at least once.

YNAB is the correct choice if your goal is behavioral change and you will actually follow the methodology. The abandonment risk is real, but the outcomes for users who stick with it are the strongest in the category.

Avoid switching apps every time a new review appears online. Every budgeting app requires weeks of transaction history before its AI delivers accurate recommendations. The "budgeting app burnout" cycle (migrate, recategorize manually for two weeks, switch, repeat) is self-defeating.

Frequently asked questions

Monarch Money is the most direct Mint replacement for users who want full-household financial tracking. It was built by the original Mint product team and covers net worth, investments, budgeting, and AI spending analysis in one platform. YNAB is the best alternative if you want behavioral change through zero-based budgeting rather than automated tracking.

Most apps connect through Plaid, which uses tokenized access (not your raw credentials) and read-only permissions for tracking features. Plaid covers 12,000+ financial institutions and uses AES-256 encryption. The real tradeoff is that Plaid retains transaction data on its servers. Apps with auto-save features (Cleo Autopilot, Rocket Money) also require write permissions scoped to savings sweeps. If you want no cloud exposure, Finny and SenticMoney are local-first alternatives.

OpenAI launched a Plaid bank connection for ChatGPT Pro subscribers in May 2026. The difference from dedicated budgeting apps is reasoning capability. Purpose-built apps answer fixed questions (what did I spend on dining?). ChatGPT with Plaid can answer open-ended ones (what is the optimal way to allocate $3,000 given my current debts and upcoming expenses?). The limitation is price: $200/month for ChatGPT Pro puts it out of reach for most users as a budgeting tool.

Yes, for categorization quality. Copilot's per-user AI model achieves approximately 93% first-pass accuracy and learns from corrections in a way that genuinely reduces manual cleanup over time. At $95/year it is priced lower than Monarch Money Core. The constraints are no Android, no Windows, and no couples support. If your household is all-Apple and single-user or two iPhones with separate accounts, it is the best categorization experience available.

Monarch Money is the strongest couples platform. It supports shared dashboards with joint and individual account views, collaborative financial goals, and separate spending visibility for each partner. Origin also includes couples access at no extra cost and adds retirement projection and investment analysis. YNAB supports couples budgeting through its zero-based framework but at a higher engagement cost.